This article is also available in Japanese.

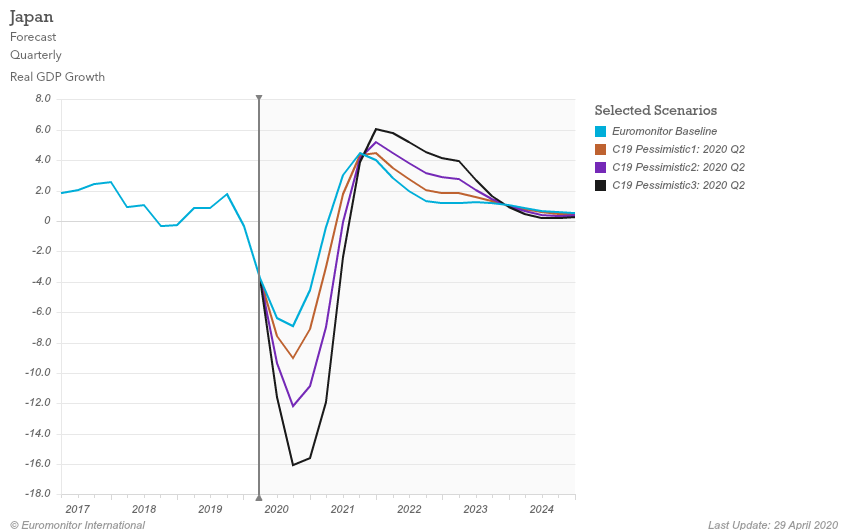

Japan began 2020 with optimism for a new start, following economic and literal headwinds in Q4 2019, with all eyes set on the country in the lead-up to the Tokyo Olympic Games. Instead, at the turn of the new year, Japan welcomed some of the first cases of what turned out to be a global pandemic, resulting in the March decision to postpone the Olympics until 2021, the first time in history. Despite no compulsory lockdown in Japan, businesses and residents took many precautionary measures to safeguard against the Coronavirus (COVID-19) outbreak. Fortunately, a more devastating public health crisis and immediate economic impact seen in other countries has been largely avoided in Japan to this point. However, the impact of the shifts in business operations and consumer behaviour will soon bring financial hardship. This, combined with the lasting psychological impact of the recent COVID-19 scare, will shape future consumer decisions.

Source: Euromonitor International Macro Model

This follows a difficult end to 2019 in October. A combined blow delivered by a long-delayed VAT increase from 8% to 10% and record damage caused by a series of typhoons rattled the economy and consumer sentiment. The tax hike dented already price-sensitive consumer expenditure, while the storms disrupted economic activity and forced a massive stimulus package to support recovery.

As a result of COVID-19, 7 April marked the declaration of a state of emergency in the most affected areas that eventually spread to cover all 47 prefectures. The state of emergency started to get lifted from the middle of May, first in prefectures that had fewer cases, and then finally on 25 May, the state of emergency was lifted on the remaining prefectures that included the country’s capital and economic hub Tokyo.

Euromonitor’s Japan team of industry experts explores the impact of COVID-19 across five groupings of fast-moving consumer goods and services industries with a focus on the impact of home seclusion, channel shifts and preventative health.

Food and Nutrition: Now playing a larger role in daily life with health and convenience in high demand

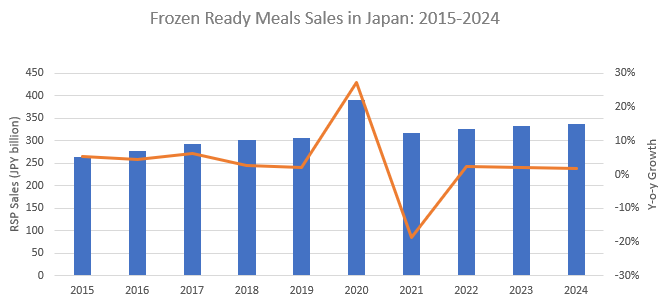

Everyone’s a home cook now: Due to work from home, school closures and home seclusion, Japanese started preparing and eating at home more frequently. This led to the sudden growth of time-saving packaged food products particularly frozen ready meals and cooking sauces that help consumers to prepare meals faster and easier. Japan has a traditional business culture that has largely limited work from home until COVID-19 made it a new option for millions of workers. It is likely that working from home will gain more widespread acceptance in Japan even when the threat of COVID-19 diminishes. Manufacturers of quick-to-prepare packaged food should seize this opportunity to meet the potential new demand, not only for work from home, but also as Japanese consumers may tend to stay at home and avoid foodservice at least in the near term.

Source: Euromonitor International. Note: Historic current prices, forecast constant 2019 prices

Normalisation of rolling stockpiling: Japanese people are stocking up on shelf stable products such as noodles, pasta and canned foods due to the concern over COVID-19. Panic buying that was seen when the government’s stay-at-home recommendations were made in April will happen less and less as the COVID-19 situation returns to normal. However, COVID-19 has accentuated the home stockpiling trend for disaster prevention that was already common in Japan due to frequent natural disasters. It is expected that despite the small space of the typical Japanese home, consumers will increasingly stock staple packaged foods on a rolling basis for peace of mind.

Online grocery sales go local: As consumers stay at home the convenience of online grocery shopping has seen a recent surge in demand. It is expected that consumers who used to hesitate to purchase groceries online before COVID-19 will shift their shopping preference to now also include online purchases to supplement store-based shopping even after the COVID-19 situation dies down. Particularly, online platforms that sell agricultural products directly from rural producers, such as Tabechoku, are gaining popularity as consumers look to support small businesses such as these that are negatively impacted by COVID-19. This movement to support local businesses was also seen after the 2011 Great Earthquake.

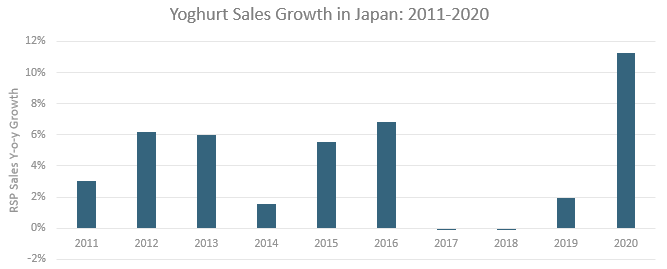

Preventative health top of mind: Residents want to strengthen their immune system to prevent COVID-19 infection, and there is an increasing demand for health and wellness food such as yoghurt, which successfully reversed the downtrend since 2016 to hit record high sales in 2020. Manufacturers are addressing the increased at-home consumption by launching bigger packaged products, such as seen by the recent success of the R-1 functional probiotic yoghurt brands by Meiji. Japanese consumers are typically very health conscious and COVID-19 has boosted the demand for food that offers preventative health.

Source: Euromonitor International. Note: Historic current prices, forecast constant 2019 prices

Drinks: Catering to new at-home consumption experiences and increased health awareness

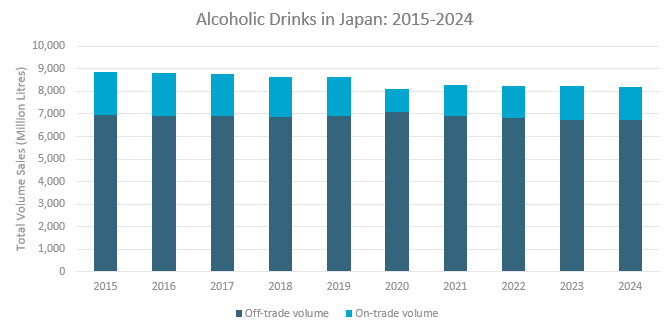

Boost from home drinking: Despite no enforceable hard lockdown, many foodservice outlets voluntarily closed following the requests from municipalities. Even as restaurants adapted to offer takeout or delivery service, demand for alcoholic drinks has plunged. Going forward, foodservice operators must create safe dining environments and unique drinking experiences to bring back customers, otherwise many people will choose to continue drinking at home. “Online nomi” (online drinking session) has been widely accepted across various generations during the stay-at-home period. This trend is further supported by record sales of RTDs that come in myriad varieties to cater to all consumer segments. This trend should continue even after the COVID-19 situation dies down as the economy takes a hit and consumers will be more budget-minded.

Source: Euromonitor International

Polarised demand: Similar to what happened after the 2008-2009 Global Financial Crisis, despite consumers becoming increasingly budget minded, they are still looking to treat themselves. During the recent COVID-19 outbreak in Japan, the cheaper options of economy lager and RTDs have posted good results due to at-home demand, while mid-priced lagers are struggling. On the other hand, some stay-at-home consumers are translating their savings on foregone dining-out experiences to trade up on their retail drink purchases. For example, Japanese craft brewers such as Yoho Brewing have rushed to increase shipments to keep up with surging retail sales.

Increase in awareness for self-maintenance: Daily consumption of beverages with health and wellness benefits has been on the rise in Japan. Now thanks to increased preventative health consciousness due to COVID-19, immune-enhancing and stress-reduction beverages are in higher demand. Drinks with functional ingredients or health-boosting claims such as iMuse Water by Kirin with Lactococcus Plasma will continue selling well as we expect to see rising demand for products that are both healthy and refreshing.

Bulk sales boom: Drinks in larger pack sizes are on the rise. The state of emergency declaration asked citizens to limit daily grocery shopping to once every three days to minimise human interaction and their risk of falling ill. This resulted in the expansion of at-home-friendly larger pack sizes. Especially bulk sales of bottled water are becoming more common also as an ingredient due to consumers shifting to prepare coffee and tea at home, as well as the increased frequency of cooking at home. On the other hand, with people refraining from going out, on-the-go impulse purchases of smaller pack sizes have plunged especially for drinks such as RTD coffee, carbonates and sports drinks. Online drink sales look to have a defining moment now to enter a new phase of distribution to accommodate consumers’ behavioural change. Still challenging for manufacturers is how to boost online drinks case sales due to the small size of dwellings in Japan. Manufacturers can look for ways to appeal to consumers’ needs perhaps through subscription services of variety packs.

Home and Technology: Attending to consumer struggles adapting to the merged house and office life

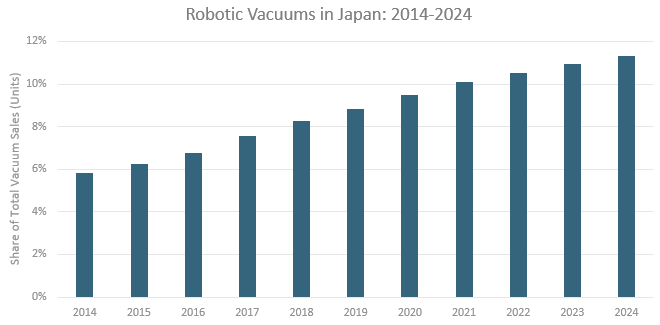

Home help: The burden of household chores has increased during COVID-19, and appliances that help people save time will benefit. Fully automated combination washing machines and dryers, robotic vacuum cleaners and automatic dishwashers are in demand. Time-saving small cooking appliances such as bread makers and electric grills have been on the rise as consumers limit their foodservice experiences. Working from home was not well accepted in Japan’s traditional business culture. Thanks to COVID-19, attitudes have become more progressive so many people started working from home for the first time, resulting in strong demand for equipment and products to set up an effective home office environment. External monitors, printers, work desks/chairs and room air fresheners have benefited.

Higher demand for hygiene: People are now more concerned about caring for their health and are interested in products with disinfectant and antibacterial effects. Examples include hot water washing machines (cold is the norm in Japan), detergents with bleach, disinfectant wipes and kitchen cleaners with antibacterial properties. Air treatment products have also been on the rise as consumers spend more time at home and look to prevent airborne pathogens and contamination that may lead to reduced immunity or illness.

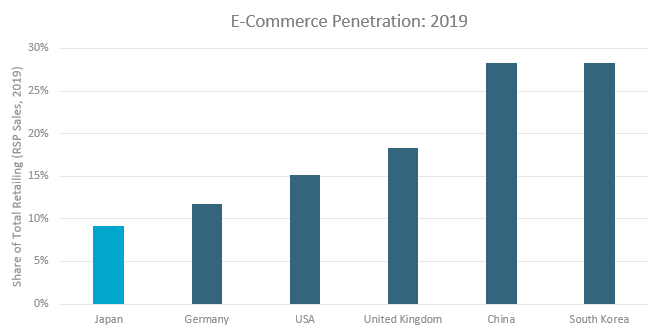

Hard hit by store closures: E-commerce has helped pick up the slack as retailers quickly pivoted their sales model. This will cause a long-term change in retail distribution structure, especially for home care and tissue and hygiene products that are still heavily dependent on in-store sales through drugstores. This should provide an opportunity for more direct-to-consumer specialised brands and small and medium-sized brands to connect with consumers via digital marketing and social networking services.

Source: Euromonitor International

Service and Payments: Accelerating advancement due to faster consumer digital uptake

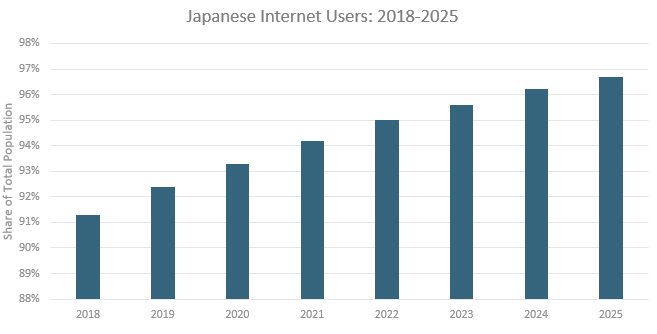

Diversification of channels: Despite its high-tech image, service and payments in Japan continue to have strong traditional roots. Thanks to the rapid shift spurred by COVID-19, it is expected that consumers’ digital adaptation will advance, and distribution channels will further diversify. Stay-at-home requirements saw retailers, foodservice and other businesses reliant on face-to-face business close outlets or shorten business hours. On the other hand, online sales, delivery and take-out channels are growing. Consumers who were not familiar with online services such as restaurant delivery applications before COVID-19 are now experimenting with these technologies. After getting over the initial technological hurdle and potential concerns of handling of personal information, Japanese consumers are likely to continue using such convenient services. Similarly, digital payment options should receive a boost from the desire for reduced contact shopping experiences in-store.

Source: Euromonitor International

Changes in business customs: COVID-19 has drastically impacted how we work and travel. Video conference services and working from home have quickly become more common. Lodging and airlines that cater to business travellers will need to provide assurances about customers’ safety as well as incentives to travel. Looking ahead, it is likely that pure business trips will be reconsidered now that technology can provide both cost savings and protection from infection. On the other hand, the concepts that have been less common in Japan - such as workcation - that can add a new angle to the purpose of business trips, have potential to grow in the coming years.

New digital experiences: While many companies and industries are facing difficulty maintaining in-store sales due to COVID-19, new digital services offering augmented experiences will see opportunity. These technologies should help brands connect with consumers who still desire to try a product before making their purchase decision but prefer to avoid crowded in-store experiences. This also applies to experiences and entertainment, where companies have been testing virtual travel and virtual sporting event viewing by utilising VR and 5G technologies.

Source: Euromonitor International

Beauty and Fashion: Adapting to fundamental shifts in market dynamics

Dilution of seasonality: Sales of spring and summer apparel lines have been badly affected by COVID-19. Traditionally, the apparel industry updates seasonal portfolios every six months, however, the biannual replacement demand for apparel was already declining in Japan before COVID-19 due to the rise of the circular economy and sustainability trends. After COVID-19, it is expected that durable fashion items that maintain their resale value will gain even more popularity over seasonal and trendy products. The expected economic recession in 2020 will only accentuate the pre-existing cost-conscious consumer behaviour and how they perceive the value of clothing and footwear.

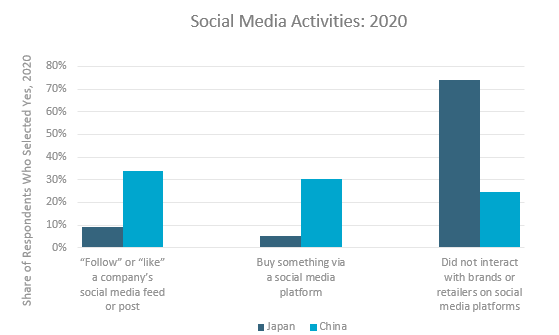

Digital shopping experiences: According to Euromonitor’s 2020 Global Consumer Lifestyles Survey, before the COVID-19 outbreak Japanese consumers were not actively engaging with brands online or through SNS, but the COVID-19 outbreak emphasised the importance of direct communication with fashion brands and their customers. This is particularly important for senior consumers who account for nearly one-third of the population in Japan and used to enjoy fashion shopping at department stores with extensive customer service. Going forward, it will be important for brands to strengthen usability and functionality of their own e-commerce sites to offer an enhanced and smooth shopping experience and keep customers engaged with the brand directly rather than relying on online marketplace platforms.

Source: Euromonitor International Lifestyles Survey, fielded January to February 2020

Preventative health in doubt: In recent years the Japanese government has promoted treating minor health ailments with over-the-counter consumer healthcare products. However, due to the uncertainty of COVID-19 symptoms and the potential severity of a diagnosis, Japanese consumers are opting to rely on expert medical examination and prescription medicine over self-medication. On the other hand, sales of vitamins and dietary supplements have benefited due to growing consumer awareness of preventative health focusing on daily immune system.

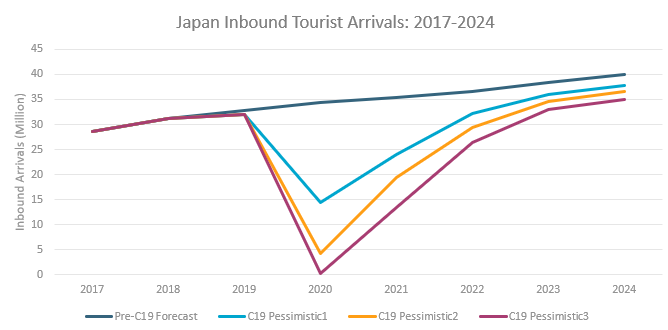

Domestic demand for beauty growth: Japan’s beauty and personal care market has been heavily reliant on inbound tourism demand to maintain growth. Whether the inbound tourists can or will come back to Japan, and if they continue to splurge on retail beauty products to take back home, will have a substantial impact on the local industry. Japanese beauty manufacturers will need to reduce dependence on inbound sales and generate demand among local consumers.

Source: Euromonitor International Travel Model

COVID-19 disruption will spur Japan to evolve by relaxing culturally ingrained habits

The impact of COVID-19 on Japanese consumer trends and lifestyles has been rapid and profound. What is evident is that the key trends are largely an acceleration of existing ones. The abrupt shift in consumer habits as a result of COVID-19 has led to increased time spent at home with a more open acceptance towards a fluid work-life balance. It has also pushed the uptake of digitalised commerce that has been stubbornly and paradoxically lagging in Japan compared to its peers. Known for its people’s longevity and balanced diet, Japan now looks to embrace an even greater focus on preventative health. Economic recession will create sales growth challenges and the prospect for a resurgence in new COVID-19 cases still looms. Lessons learned from the recent episode will help brands find opportunities and look for ways to connect with consumers who are now demonstrating greater adaptability during these uncharted times.

This analysis was prepared by Euromonitor’s Japan team of research specialists:

• Megumi Matsunaga

• Nozomi Hariya

• Sachi Kimura

• Sean Kreidler

• Taro Yamato

• Tatsunori Kuniyoshi

• Tomomi Fujikawa

• Yuri Gorai