Whilst the global unbanked population has been decreasing substantially over the last five years due to consumers having increased access to financial services, there are still billions of consumers who have not adopted formal financial services.

This article highlights the growing disruption of the traditional card and electronic payment landscape from technology companies, mobile network operators and others all offering alternatives to mainstream financial services providers.

Consumer payment policy coming into focus

Governments around the world are more aware of the benefits of moving to a cashless society. There is also a better understanding of the positive economic impact financial inclusion can have, prompting measures to lower the barriers to financial products and services.

Several markets have reduced the regulatory requirements for financial service providers and payment processors allowing for greater competition from technology, mobile network operators and social media companies.

The success of online-only banks offering low-cost financial services in emerging markets has brought millions of consumers into the financial services fold.

There were 137 million more banked consumers over the age of fifteen in 2017–2018, bringing the global total to 3.5 billion. 2018 marked the first year when the financially underserved population decreased in terms of total population.

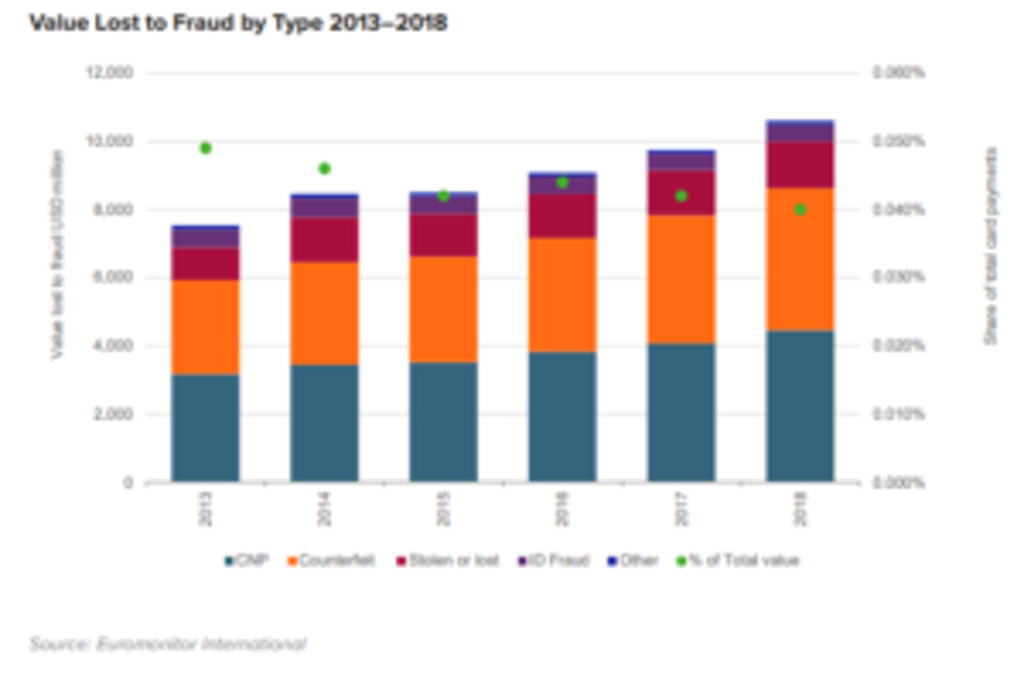

Fraud value grows despite innovation

The total value lost to fraud on card transactions across the 47 markets researched increased by 9% over 2017–2018. This was largely due to an increase in the US, which accounted for 59% of that total value in 2018.

The shift to chip cards in the US was a measure aimed at curbing counterfeit card fraud, but even that category increased by 12%. The absolute value of card fraud in the US reached USD6.5 billion in 2018 from USD3.9 billion in 2013.

The two largest fraud categories globally by value in 2018 were counterfeit card fraud and card not present (CNP), accounting for 44% and 41% respectively. As a share of total card payment value, value lost to fraud was greatest in Mexico followed by Nigeria, Colombia, Vietnam, Australia and the US.

M-commerce value to grow 250% over five years

M-commerce in the 47 markets researched by Euromonitor International is expected to increase from USD1.9 trillion in 2018 to USD4.3 trillion by 2023. Growth is being driven by consumer adoption in the US and China, which combined are projected to account for 75% of m-commerce growth in the 47 markets.

Widespread adoption of smartphones as well as the capabilities of the devices has changed the way consumers research, shop and purchase products. The conversion of retail has enabled non-traditional technology companies access to the payment landscape.

Despite investment in proximity mobile payments, the growth of m-commerce is expected to be on remote channels primarily. However, as a share of total m-commerce, proximity payments are expected to increase from 17% in 2018 to 28% by 2023.

To learn more about the growing disruption of the traditional card and electronic payment landscape download our white Global Consumer Finance Landscape: Trends Disrupting Payments.