This article is part of a series on COVID-19 focusing on how the outbreak is affecting industries.

As the coronavirus (COVID-19) incidence advances in Brazil, economic fallout and major impacts are expected in different consumer goods and services industries. This comes not long after industries were showing signs of recovery following the country’s economic crisis in 2014-2018.

Euromonitor International forecasts another year of negative real GDP growth for Brazil in 2020. While we foresee some categories benefiting from spikes in short-term demand, most industries foresee major negative impacts on sales in 2020. This is especially true in services industries, where consumption occasions that did not take place due to the lockdown cannot be made up in future consumption events.

Regardless of the industry, however, important common denominators should drive consumer behaviour in Brazil over the next few months:

• Bottlenecks in production chains and distribution: Reduced workforces may create or worsen pre-quarantine scenarios;

• Sales concentration in some industries in Q1 and Q2 2020 may not be sustained throughout the whole year: The level of product inventories is unprecedented for Brazilian industry, and manufacturers were not prepared to manage unexpected production;

• Reframing of consumption occasions: While there are new occasions boosting demand for products like streaming and video games, others, like restaurants, hotels and entertainment, are being harmed by lost opportunities;

• Resistance test for retailing: Omnichannel structures have become more important than ever and will consistently be tested in a scenario where non-essential stores must remain closed;

• First things first: Prioritisation of essential items may offset the timid signs of recovery many industries were trying to accomplish after the economic crisis in 2014-2018 – the result of unsustainable government expenditures, political instability and economic model failure.

Unemployment and confidence levels are the key indicators of Brazilian market resilience

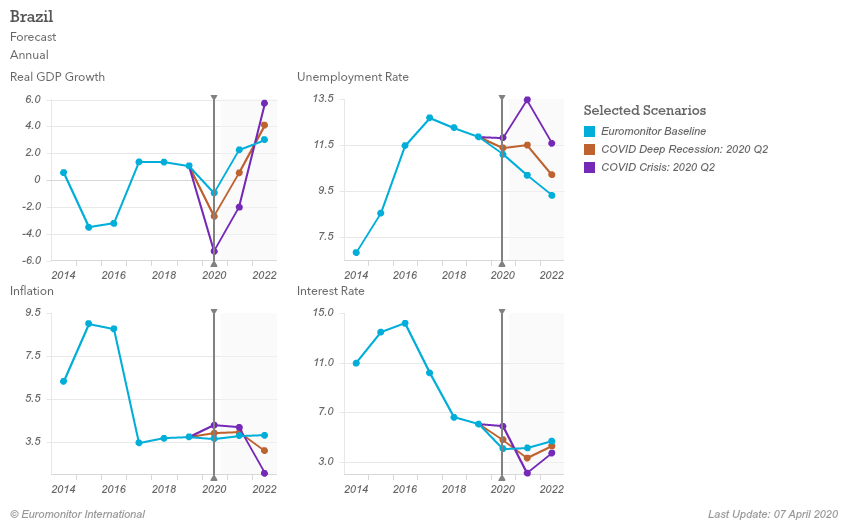

According to Euromonitor International’s Macro Model, the impact of COVID-19 on our baseline forecast for Brazilian real GDP will lead to a decline of 1.0% in 2020, while the impact of a COVID-19 Deep Recession would lead to a similar downturn to that seen during the crisis of 2014-2018.

If a COVID-19 Crisis scenario consolidates, however, unemployment rates and real GDP growth will be significantly worse than in 2016 (the worst year of the crisis), leading the Brazilian market to generally collapse. The Latin American outlook will be subject to further downgrade revisions if COVID-19 outbreaks worsen.

Potential Macroeconomic Scenarios Due to COVID-19: Deep Recession and Crisis

Source: Euromonitor International Macro Model

Beverages: prioritisation of essential items

As the COVID-19 outbreak intensifies in Brazil, consumers are returning to “crisis mode”, copying many habits acquired during the economic crisis of 2014-2018. This means prioritisation of essential items, especially due to concerns about unemployment.

Bottled water and coffee are set to see the greatest rises in demand in the short term, especially through larger pack sizes, as these are considered essential items for most Brazilians, who are looking for the most affordable unit prices. In the case of bottled water, bulk sales are expected to offset volume declines seen in the last couple of years, while intermediary packs (5-8 litres) should continue to grow in volume terms.

Spirits, however, might struggle. On-trade establishments will suffer the biggest impact due to mandatory lockdowns in major cities, which are set to be followed by others in the coming weeks. Such a scenario might have a negative impact on ever-rising volumes of gin and recovery of vodka, previously boosted due to the popularity of Gin & Tonic and Moscow Mule cocktails respectively.

Additionally, the US dollar exchange rate has reached BRL5.0, compared to a previous rate of BRL4.49 before the first case was confirmed on 26 February 2020, with a significant impact on prices of imported drinks, mainly spirits and wine.

Packaged food: sales concentration on non-perishable items in Q1 and Q2 2020

Packaged food will undoubtedly benefit in the short term, as consumers are staying at home and replacing “eating out” occasions with homemade food. The most important items have been staples (rice, pasta and sauces/condiments), shelf-stable vegetables (the first items that supermarkets set purchase limits on), frozen ready meals and snacks. In general, products with longer shelf life are preferred during the quarantine, while chilled products such as yoghurts and ice cream are not considered cost beneficial at this point.

Such a positive scenario in the short term, however, does not necessarily mean peaks in year-based sales in the second half of the year due to leftovers of longer shelf-life products. Other challenges are distribution logistics affected by a reduced workforce, raw materials shortage (especially those which are harvest dependent) and bottlenecks in packaging supply, as with glass manufacturers, for instance.

Technology and connectivity: digital services rise at the expense of technology-based products

With quarantine stipulated in most states in the country, digitalisation and online commerce and services have been greatly favoured by the “stay-at-home policy”, with both e-commerce, delivery and streaming platforms seeing a surge in demand. It will also strengthen online adoption and mitigate concerns surrounding digital consumption in the long term, which are still quite common in Brazil.

On the other hand, technology-based products – like smartphones, wearables and other small consumer appliances – have felt the COVID-19 blow, with the first quarter forecasting retraction within the industry. This is because of reduced production and distribution efficiency (due to a reduced logistics workforce), fewer import products making their way from China, postponement of product launches and devaluation of the Brazilian currency, increasing manufacturing and import costs.

However, there are outliers to this scenario, such as computer peripherals (as more people adopt home office standards), food preparation appliances and video games.

Home care and hygiene: intensification of home care and focus on basic hygiene products

As replication of other countries’ scenarios, toilet paper has become one of the main demanded products in the weeks of quarantine in Brazil, resulting in disruptions of supply and availability in many grocery stores.

While the unforeseen spike in the short term should not reflect a peak in year-based volume sales for the category, such strong demand in Q1 should contribute to concentrated production and distribution efforts for this category. As many consumers already stocked significant volumes of toilet paper, positive performance should be followed by a sales drop as the situation stabilises.

In the week after the first COVID-19 case in Brazil in February 2020, general home cleaning products already presented significant volume sales rises, in anticipation of the quarantine period. Concerns with home cleaning and personal hygiene are high, benefitting sales of dishwashing items (as more people cook and eat at home), bleach and surface care. However, for these categories, a year-based volume sales increase is expected as consumers are developing the habit of cleaning their households more frequently.

Fashion: one of the Brazilian sectors most impacted by lockdown

If the slow-paced growth of fashion categories was a concern related to the weak macroeconomic indicators in Brazil over the last couple of years, the pandemic scenario represents a big shock. Apparel, footwear, personal accessories and eyewear have been completely deprioritised at a time when most families are focused on stockpiling food and hygiene items.

As fashion categories’ operations are strongly concentrated in physical channels, and the main retailers are closing all their stores for an undetermined period, expectations rely on the quarantine duration to foresee when and how the industry can minimise impacts.

In the first semester, Mothers’ Day sales (celebrated in May) are expected to be severely harmed. In the best-case scenario, a shorter return to fashion categories’ pre-COVID-19 sales level in 2-3 months would bring possibilities for recovery in Q2. Retailers are already engaged in negotiating sector agreements with the federal government to reduce costs (taxes and rental fees) to soften the losses.

Beauty and personal care: distinct scenarios based on the essential nature of products

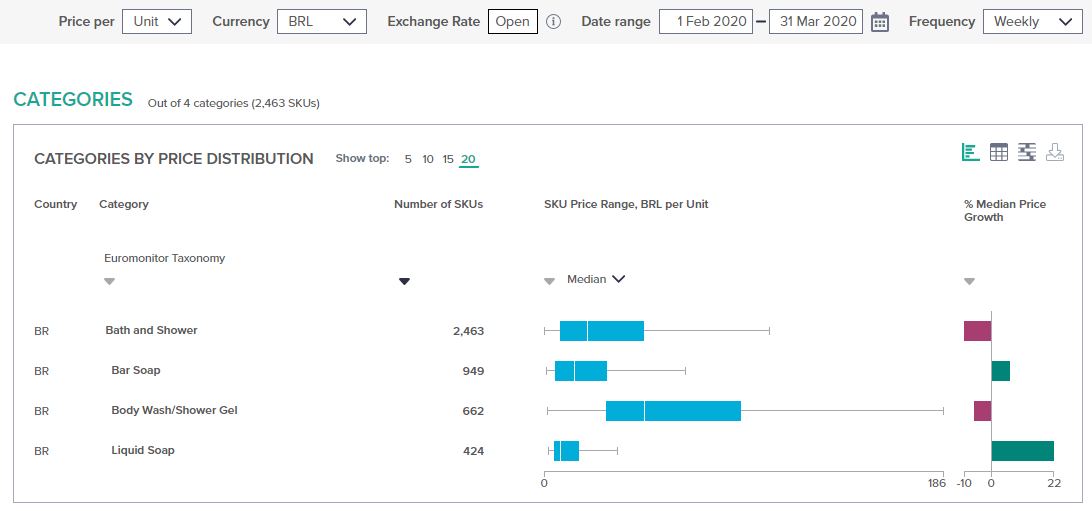

COVID-19’s impact on the beauty and personal care industry will mostly present two distinct scenarios. In the personal care space, sales should not present a negative performance. In fact, sales of categories such as bath and shower are expected to grow in the short term, with many consumers looking for items such as bar and liquid soaps.

According to Euromonitor International’s price tracking system, Via Pricing, sales of liquid soap presented over a 20% weekly price increase between February and March 2020, showing the effects of high demand for items considered essential to prevent contamination.

Bath and Shower Items: Weekly Price Variations During COVID-19 Scenario

Source: Euromonitor International Via Pricing system. Note: Prices in BRL, from 1 February 2020 to 31 March 2020, weekly basis

As for beauty-related items, a different scenario is expected. With several consumers staying at home, categories like colour cosmetics and fragrances are expected to perform poorly, as these are usually related to “going out”. Due to lost “going out” occasions during the quarantine, sales of these products should not see a year-based recovery. Together, these two categories represent almost one-third of total beauty and personal care value sales in Brazil, potentially contributing to negative overall sales for the industry in 2020.

Consumer health: consumers look for immune system-boosting solutions

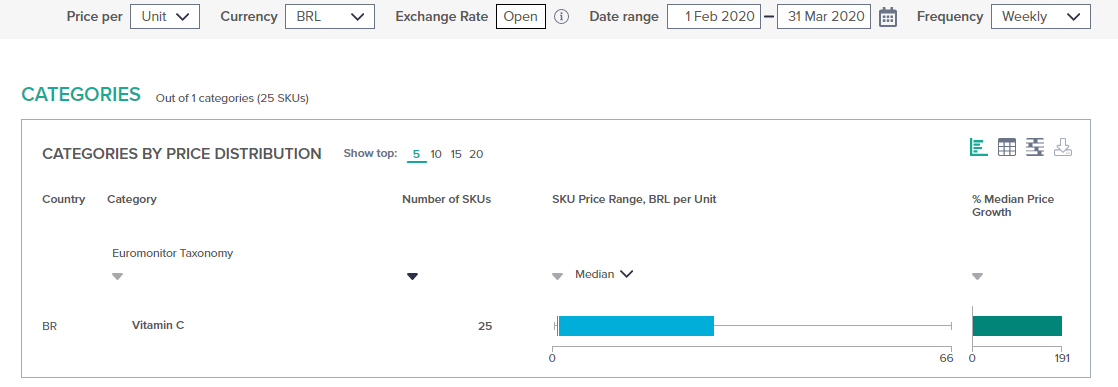

Consumer health is one of the few industries to have been boosted by the outbreak. Consumers rushed to drugstores aiming to purchase all sorts of products that claim to boost immune systems and potentially target COVID-19 symptoms. Items such as Vitamin C, multivitamins and even natural products such as propolis were hardly seen in many outlets from the beginning of March onwards.

Since confirmation of the first case in February, prices have soared in the country. Vitamin C, for instance, posted a growth rate of almost 200% on a weekly basis, from February to March 2020, according to Euromonitor International’s Via Pricing system. However, with the heated demand, there might be a lack of important raw materials to sustain production and supply in the medium term, potentially offsetting short-term positive results throughout 2020.

Immunity-System Boosting: Weekly Pricing Variations During COVID-19 Scenarios

Source: Euromonitor International Via Pricing System. Note: Prices in BRL, from 1 February 2020 to 31 March 2020, weekly basis

Services: government help needed to maintain service sectors in 2020

Unlike goods, which consumers can buy after the crisis, services such as travel and tourism and consumer foodservice will not benefit from the recovery of pent-up demand. The consumer foodservice industry expects the government to announce a package of emergency measures, capable of bearing a monthly benefit to restaurant workers for the next three months, to prevent mass layoffs.

Although delivery activities are still allowed, even in cities where a quarantine has been established, the delivery market in Brazil is composed mainly of independent players that rely on delivery as a complementary operation, making it insufficient to compensate for the loss of revenues associated with the closure of dining areas. Therefore, although players are looking for diversification into delivery options, most of them do not have delivery operations that are robust enough to rely only on delivery activities.

Retailing, in turn, is seeing heated activity for most grocery channels, as well as for drugstores and pharmacies. However, nearly all other store-based channels are expected to face months of sales at record lows. Players which demonstrate greater robustness in their operations in digital channels, both in terms of user experience and logistics operations, will be able to mitigate part of the impact of the lockdown. E-commerce represented 8% of total Brazilian retailing value sales in 2019, with this ratio expected to increase in 2020 as the crisis boosts demand for this channel. Digital payments are expected to benefit from this movement as well.

Lastly, the travel and tourism industry sees a much less encouraging outlook. With about 80% of lodging players closed and all parks and tourist attractions have had operations suspended, the industry expects the government to help pay employees’ salaries within the next few months. According to trade association estimates, tourism in Brazil could lose around USD6.2 billion without the support of government aid. Euromonitor International’s Travel Industry Forecast Model expects that the baseline scenario for inbound arrivals to Brazil will decrease by 50% in 2020, while the deep recession scenario presents a 54% decrease for the category in the same year.

The following specialists contributed to this report:

• Angelica Salado

• Elton Morimitsu

• Guilherme Machado

• Marcel Motta

• Marília Borges

• Pedro Alves

• Ricardo Sfeir

• Rodrigo Mattos