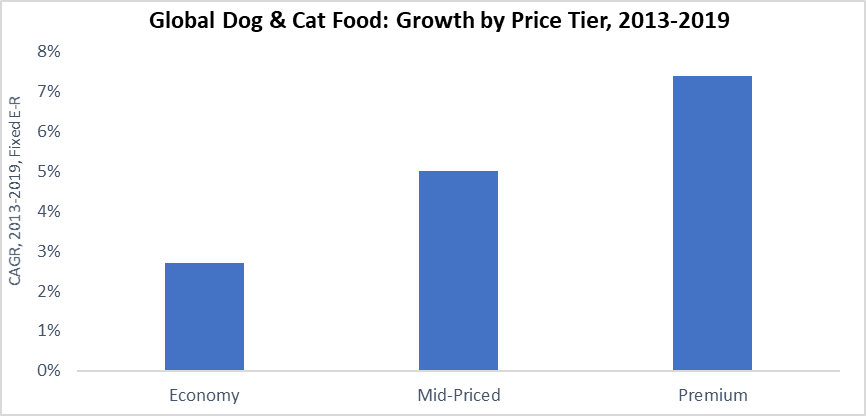

In a rapidly-urbanising world, the growing popularity of smaller dog breeds has made it difficult to grow pet food volume sales. In fact, volume growth in dog and cat food has not topped 3% globally for at least a decade and a half. In this environment, rising average prices – driven by pet humanisation trends – have been the foundation of industry growth.

As owners are increasingly willing to spend on premium, high-quality food to improve the health and wellbeing of their pets, trading-up has helped increased average unit prices by nearly 24% across dog and cat food from 2013 to 2019.

Ingredients as the historic driver

For decades, ingredients have been the primary battleground in premium pet food. Ingredients serve as a primary source of brand differentiation, and ingredient-focused messages dominate brand marketing.

Ingredient trends have evolved over time. In the early 2000s, the focus was on the scientific engineering of ingredients to optimise recipes for specific life-stages. Iams Premium Protection, for instance, used veterinary and nutritional science to create an optimal food for puppies.

Premium pet food saw a tidal shift in the 2010s. Upstart brands like Blue Buffalo encouraged owners to take the “True Blue Test” and examine the top five ingredients in their pet’s food. Natural, meat-first and ancestral diet recipes exploded in popularity as transparency assumed new importance.

Despite this shift, ingredient composition remained at the centre of premium pet food. For decades, this overarching focus on product formulation has not wavered.

Moving away from processed food

As the industry moves into a new decade, premium pet food is on the precipice of a transformational shift. Owners are moving beyond ingredient lists to gauge the physical appearance of pet food. In many ways, the processing method used to create pet food is becoming as important as the ingredient list.

This change is rooted in broader dietary shifts. Processed food has fallen out of favour as consumers gravitate towards chilled or refrigerated offerings that maintain a “fresh” or “less processed” image. Across the supermarket – from dips and ready meals to breakfast cereals and snack bars – shoppers increasingly view dry, shelf-stable and centre store categories as relatively “processed”.

This poses a challenge to dry kibble – which comprised nearly 70% of the global market in 2019. As packaging in premium dry pet food increasingly features large images of fresh meat and vegetables or wilderness scenes, there is a stark and growing disconnect with the actual dried kibble product itself.

The next frontier: Pet food processing

Upstart brands are using new processing methods to move premium food beyond ingredient lists. Biologically appropriate raw foods (BARF) – in frozen or freeze-dried formats – and chilled/fresh foods claim to better maintain the nutritional integrity of ingredients destroyed by the high heat of extruding dry kibble. Raw foods more closely adhere to the format that animals eat in the wild. Fresh foods also compete on physical appearance, as evidenced by the motto of The Farmer’s Dog (US) - “Dog food should look like food. Not burnt brown balls.”

Technology is allowing these new formats to extend their reach across markets. Historically, fresh or frozen pet food required retailers to have dedicated refrigerated or freezer space – not an inexpensive proposition. And while some brands like FreshPet (USA) or Billy + Margot (Australia) have grown by building this type of retail infrastructure, technology has allowed other brands to grow in new ways.

E-Commerce has led to an explosion of direct-to-consumer brands that ship fresh food direct to pet owner doors at regular intervals. Online-only brands like DogChef (Belgium), Lyka (Australia), Pet Plate (US) and Butternut Box (UK) have sprung onto the scene. Online business models also allow for customisation with recipes designed for each pet’s specific breed, age, activity level, allergies, etc.

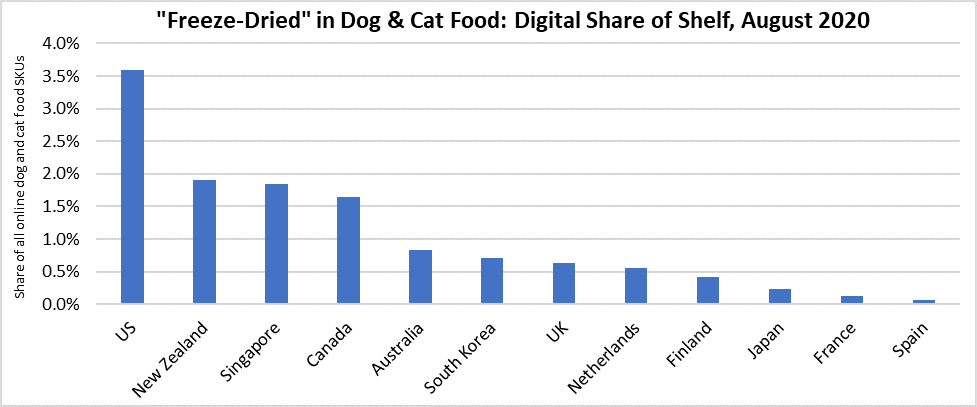

Freeze-drying technology has allowed BARF to reach new heights. In freeze-dried form, raw food becomes shelf-stable and can be sold in many more retail settings. It is also increasingly blended with kibble to provide a more affordable solution to BARF feeding. Particularly prominent in North America and Australasia at present, freeze-dried raw food is also significantly more expensive than other premium pet foods (given its low weight and high price). In fact, the median unit price for freeze-dried pet food averaged across the 12 markets below is nearly ten times higher than the category average.

COVID-19: Impact and the future

Premium pet food has proven to be incredibly resilient under COVID-19. Pet humanisation trends remain strong despite recessionary pressures, while pet ownership has jumped as people struggle with social isolation and the need for companionship. Sales of dry pet food (and processed foods generally) spiked as consumers stockpiled in early 2020 during quarantine, but this boost is likely to be temporary.

Longer-term, the future of premium pet food will increasingly be defined by physical format. Dry kibble faces threats from frozen, refrigerated, freeze-dried, fresh or chilled products that look like human food, claim to be less processed, and mirror the choices pet owners are making in their own diets.

For more insight on how COVID-19 is impacting pet care, listen to our webinar Pet Industry Insights in Light of COVID-19.