The sharp reduction in consumption occasions, the wholesale closure of on-trade establishments around the world, and the pronounced and prolonged recession that will follow the Coronavirus (COVID-19) pandemic have completely changed the operating landscape for alcoholic drinks. There will be three defining characteristics to this historic paradigm shift:

On-trade apocalypse and deciphering the “new normal”

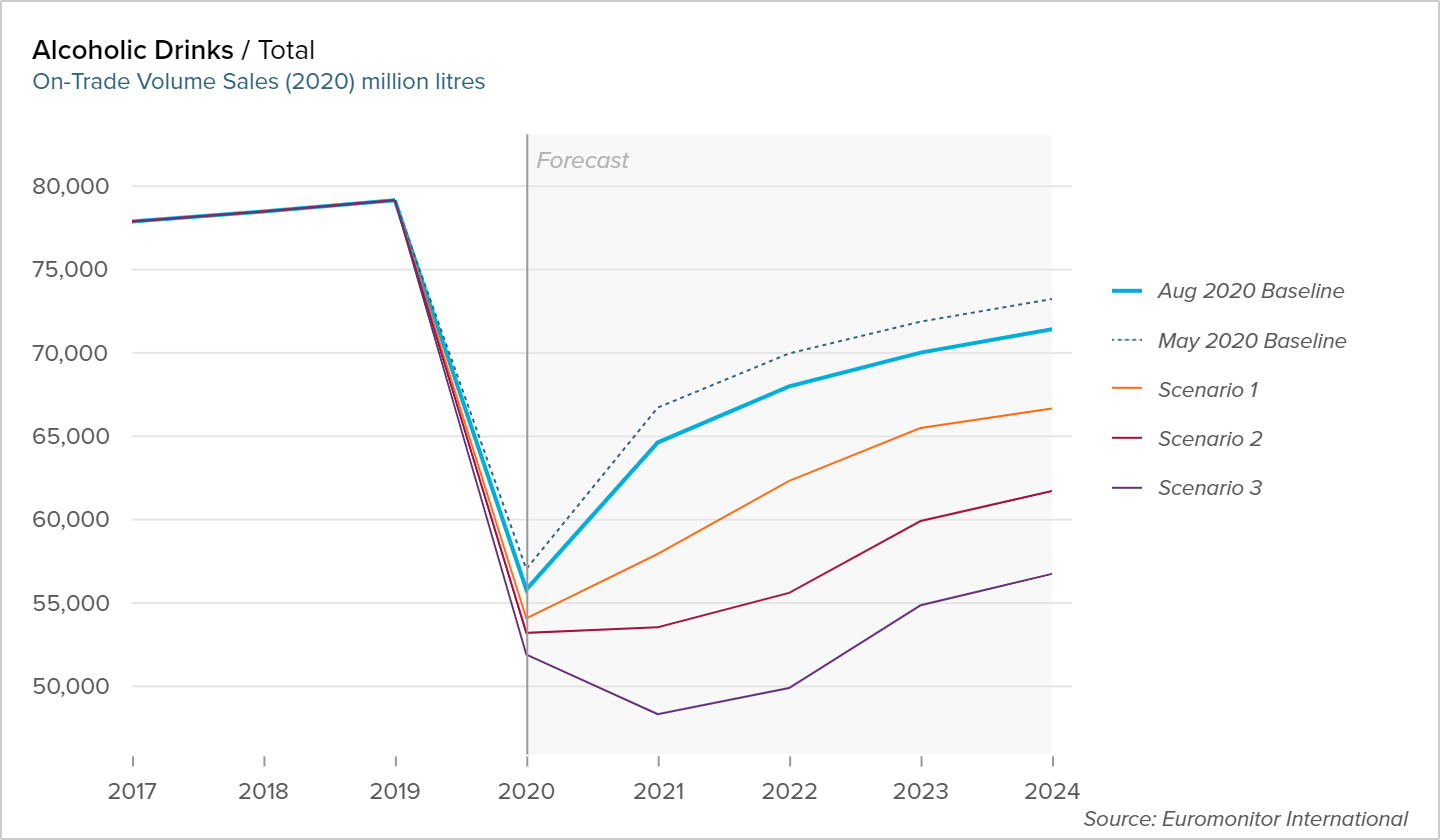

While short-term performance in bars, clubs and all other on-trade venues has been severely damaged, it is the medium to long term effects that will prove to be the most pronounced.

Source: Euromonitor International

A large number of establishments will be permanently shut following sustained losses after months of lockdown.

Those that re-open will need to radically reassess the entire experience, facilitate prolonged social distancing measures, embrace radical technological innovation and – ultimately – soften the immense sociological blow and psychological traumas and phobias that months of isolation will inevitably produce.

Operating on razor-thin margins and facing the very real possibility of second or multiple waves hitting in the short to medium term, on-trade venues will face a very precarious period, only gradually returning to full capacity.

In the absence of a vaccine or cure, a certain degree of social distancing will remain essential, with high energy occasions, clubs and live venues remaining the most challenged in the short to medium term.

Home as a shelter and entertainment hub

Countertop devices emulating the mixology or draught experience at home have been discussed for a while within the alcohol industry. Primarily embracing a premium positioning and touching upon concepts of cocooning, convenience and bridging the digital and physical realms, they offered glimpses of a future that, coincidentally, would be a perfect fit for a post-COVID-19 world.

Nevertheless, complacency, the industry’s inherently conservative nature and consumer reluctance to fully adopt such technology left some of these products in prototype purgatory or only allowed for relatively limited penetration rates. That, however, might now change.

Anecdotal information suggests that the crisis has already provided a substantial boost for sales of start-ups that have already taken the plunge, like Bartesian, a pioneer within the nascent segment of the countertop, pod-based devices replicating the mixology experience via automation.

Moving forward, the adoption of open architecture, allowing third parties to supply canisters and hence greatly increase accessibility and experimentation, will be key. Curating online recipes and creating ever-expanding online communities where ideas can be shared and virtual connections made would further cement the potential for such products.

Last orders for craft?

While the craft segment was already facing the headwinds of maturity, saturation and the inevitable softening of its once explosive growth curve, COVID-19 is likely to herald the end of the much-vaunted craft revolution.

A perfect storm of cash flows drying up shuttered brewpubs, devastated on-trade and a shift back to the comfort of established brands will lead to significant closures and consolidation.

Niche, hyperlocal opportunities will emerge, and established regional and national craft brands will cement their positions, but many mid-sized operations will fall by the wayside or potentially become acquisition targets for bigger players with strong balance sheets.

The craft segment’s core focus on the middle class and higher-income consumers should provide a certain degree of insulation from the worst effects of the crisis, and while anecdotal information suggests the segment is proving more resilient than expected in the key US market, questions remain how sustainable that is. As the economic ripple effects hit harder when financial and employment support schemes are phased out, higher-priced offerings will inevitably suffer.

Top 10 Craft Spirits Markets by Percentage Category Share 2019

| Craft’s share of spirits | Craft volume

(‘000 litres) |

|

| Brazil | 8.9 % | 63,093.2 |

| Australia | 5.5 % | 3,830.8 |

| Bulgaria | 4.8 % | 2,453.6 |

| Austria | 4.2 % | 1,169.8 |

| Canada | 3.8 % | 6,473.5 |

| USA | 3.5 % | 72,683.7 |

| Ireland | 2.9 % | 602.7 |

| Norway | 2.6 % | 336.1 |

| Belgium | 2.3 % | 589.3 |

| Switzerland | 2.3 % | 530.9 |

Source: Euromonitor International

The global alcoholic drinks market was facing saturation, increased internal and cross-category competition and shifting generational drinking habits even before the pandemic’s seismic arrival. While segments like craft provided much-needed momentum, mainstream brands were struggling to establish equity with millennial and gen Z consumers. It is within that context that short to medium-term growth will prove to be anaemic in both volume and value terms, especially as the premiumisation narrative stalls in the context of a potentially deep recession.

On the other hand, the collapse of the on-trade and resulting extreme pressures for small and medium-sized players will inevitably create opportunities for further consolidation but they will be eclectic and opportunistic, as major players will try to ring-fence their own profitability while avoiding the irrational exuberance of past cycles of M&A activity.

The industry might not be fully pandemic proof but it will prove once more that it remains adaptable and resilient.