Before the Coronavirus (COVID-19) pandemic, the global education industry was already facing various challenges, including limited educational infrastructure, a shortage of qualified educators, low public spending on education and high drop-out rates, especially in less developed economies.

The pandemic has exacerbated these issues, as over 190 countries have faced partial or full school closures due to imposed lockdown measures, affecting over 1.5 billion students globally, according to UNESCO. A deepening global learning crisis and heightened uncertainty about the future are expected to promote the adoption of digital technologies as well as encourage upskilling and reskilling of the workforce.

COVID-19 to accelerate digital transformation in education

Digital learning has emerged and evolved quickly during the COVID-19 pandemic. Education technology companies have witnessed a surge in demand due to a massive shift to online learning. Digital learning management systems, Massive Open Online Course (MOOC) platforms and other distance learning solutions have helped parents and teachers to facilitate student learning during school closures. As a result, investor sentiment regarding the edtech market is extremely positive.

For instance, in March 2020 a Beijing-based K-12 online education platform Yuanfudao secured USD1 billion in a Series G funding led by private equity firm Hillhouse Capital Group and Tencent Holdings, setting the record for the largest fundraising deal in the Chinese education market. The company runs six apps within its ecosystem and has around 400 million users already.

More online programmes from top-level universities

At the same time, the COVID-19-induced economic crisis and global travel restrictions have created challenges for international students. This may result in significant revenue shortfalls in schools, which rely heavily on tuition fees collected from foreign students. For instance, international students account for roughly 20% of all higher education students in countries such as Australia and the United Kingdom.

In order to address the issues, many education institutions, including Harvard University and Cambridge University, have decided to deliver their courses remotely at least throughout the 2020-2021 academic year and are planning to offer more study programmes that are fully online in the upcoming years.

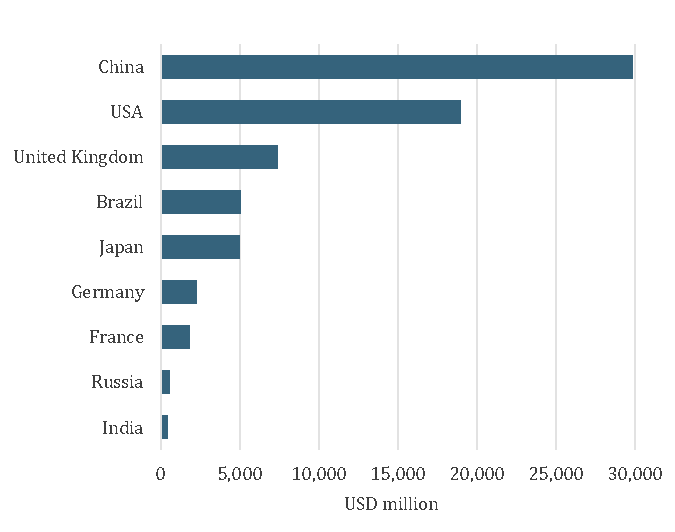

As a result, educators, especially in China, are expected to ramp up their spending on digital technologies to prevent any disruption of the learning process in future, offering vast opportunities for edtech services providers. In 2019, Chinese educators spent USD29.9 billion on ICT services, which was considerably more than any other country in the world.

Education Spending on ICT Services in Major Economies in 2019

Source: Euromonitor from trade sources/national statistics

Rising role of lifelong learning in the digital age

Continuing education is becoming increasingly important, as individuals need to readjust their qualifications amid the accelerating digital transformation and rising demographic challenges. The COVID-19 crisis has strengthened the need to enhance workforce skills. Following the pandemic, private sector companies are investing in digital training solutions, such as Lessonly, Bridge LMS and Paylocity, to upskill their employees as many of them were forced to switch to remote work.

Moreover, people around the world have lost or risk losing their jobs as a result of the pandemic. As an example, the seasonally-adjusted unemployment rate in the US surged from 3.8% in Q1 2020 to 13.0% in Q2 2020. Consequently, tech companies in collaboration with the public sector have announced various initiatives to ensure equal opportunities in lifelong learning, close skill gaps in the workforce and accelerate the global economic recovery.

For instance, Microsoft launched a global initiative which aims to foster digital skills for 25 million people hardest hit by job losses by the end of 2020. Similarly, the European Commission plans to introduce a new Digital Education Action Plan in September 2020 to promote lifelong learning in the digital age.

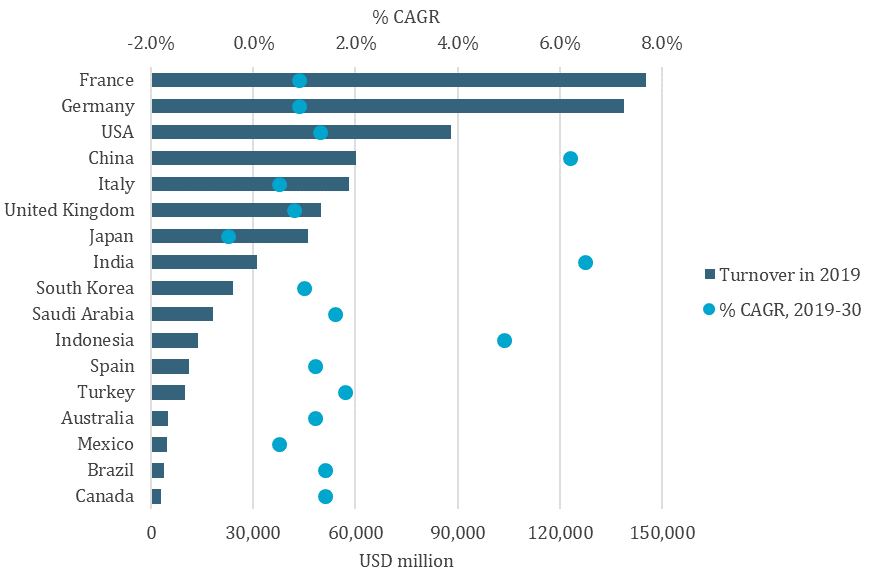

Countries According to Adult and Other Education Turnover Size 2019-2030

Source: Euromonitor from trade sources/national statistics. Note: (1) Data for 2020 onwards is forecast. (2) Forecasts are expressed in constant 2019 prices, using a fixed 2019 exchange rate. (3) Adult and Other Education includes continuing general education, continuing vocational education and provision of specialised training, generally for adults, not comparable to general education. Non-instructional services that support educational activities are also included in the category.